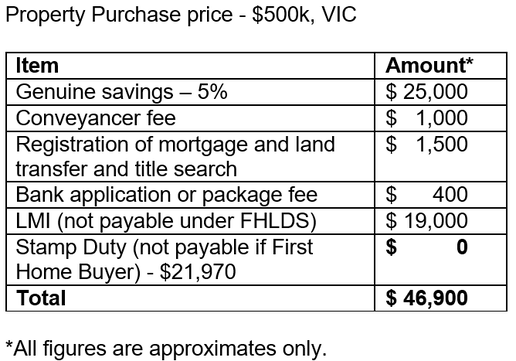

Buying your first home is very exciting. It is a big step and a huge financial commitment, so you want to get it right. Without a doubt the question I get asked the most from First Home Buyers is how much do I need to save? Everyone's situation is completely different and I am always happy to chat to you over Zoom or the Phone and discuss your unique situation. I can do some calculations for you based on how much you earn and your existing debt and expenses. But in the meantime, as a summary, here are some of the more important things to consider when saving to buying your first home: 1. You will need at least 5% of the price of the property in savings. On a $500k property that will mean you need to have at least $25k in savings. 2. Your savings need to be in your bank account for three months minimum. Savings cannot be a lump sum or gift, it needs to be gradual savings that you have had in your account for at least 3 months when you apply. This shows the lender that you can save and therefore could repay a loan. Some lenders may allow you to show rental history as quasi ‘savings’. 3. Have enough additional funds to cover fees On top of the 5% you need there will be all sorts of fees – Government registration fees, title searches, bank application or package fees and Conveyancer fees. There may also be valuation fees and settlement fees. 4. The killer is LMI The big fees are for Lenders Mortgage Insurance (LMI). If you borrow over 80% of the value of the property you have to pay this. Some lenders will allow you to capitalise (add this amount to the loan) but your interest rate will be higher. The only way to avoid this is by having a Guarantor (maybe a parent has a property they can use as security?). There has also been a recent Government initiative whereby the Government becomes the ‘Guarantor’ and LMI was not require. This was called the First Home Loan Deposit Scheme (FHLDS) – unfortunately this has finished for 2020, there were 20,000 spots allocated. They may run this program again next year, it's hard to know. I can keep you informed in you are interested as this scheme provided substantial savings as you will see in the Calculations below. Here is an example of what you need to purchase a $500k home in Victoria.  So all up to buy a $500k property you will need from $47k to over $69k (if you are not a First Home Buyer). As you can see the FHLDS is a significant saving.

Also worth noting is that the more you contribute the cheaper the interest rates will be. Repayments on $475k at 3% (estimate) are approx. $2,003 per month or $462 per week. Rates can range from 1.99% (Fixed Rate P&I) to 4.62% (Variable 98% lend P&I) so interest rates can vary hugely depending on your situation. My services are free as I am paid through the lender. So don't be afraid to ask me lots of questions. It is complicated so I am here to help. I can also take your through the various Government initiatives for First Home Buyers, some of which can save you a lot of money. There are First Home Buyer Grants, Home Builder Grants, First Home Loan Deposit Schemes and Stamp Duty Exemptions and Concessions. Some are Federally but most are State based and different for each state. I can guide you through these as well as the eligibility criteria. No question is a silly one but I do hope this give you a little insight into what or how much is required. Next time I will cover off on how much you can I borrow - the second most asked question I get! In the meantime let us work together to help you make your home ownership dreams come true. Catherine Thompson Principal, Volare Home Loans Mobile: 0411 849 804

1 Comment

|

Message from CAtherineOccasionally I come across an interesting article to do with Home Loans. I thought I'd share some of these with you here. Archives

April 2024

Categories |

RSS Feed

RSS Feed