|

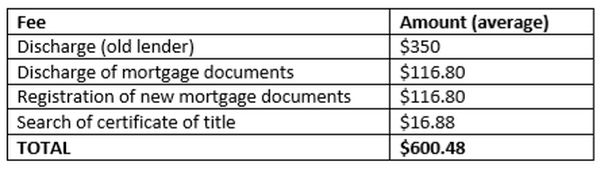

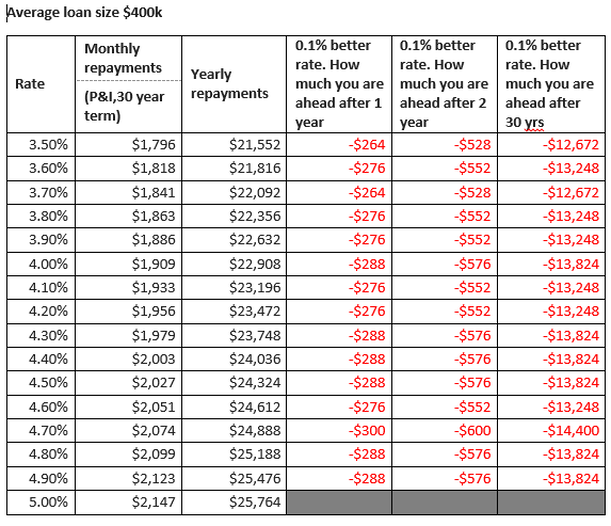

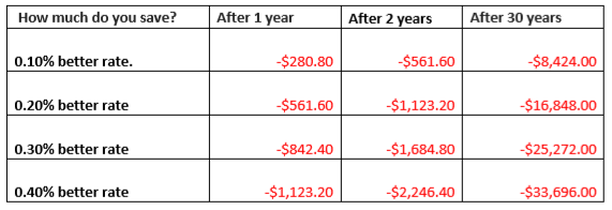

by Catherine Thompson - Principal of Volare Home Loans  Many people I talk to aren’t really sure what’s involved in refinancing a home loan. Does it cost a lot? Is it complicated? Is it worth it? Does it really save me money? If you'd like to know more, keep reading. If you don’t like reading, give me a call and I'll talk you through what's involved! Let’s start with the costs involved While the costs aren’t significant, they do exist. Most lenders will have a Discharge fee which is typically around $300-$350. Then there are Government fees of around $250. But that’s not all. There could be application fees (but not always) for the new lender and these generally range from $0-$600. Application fees often cover the valuation, legal fees and settlement fees. So, in total you need to be better off by at least $600 plus any new application fee amount to make a change worthwhile.  Now for a few more stats, according to the ABS, the average Victorian home loan is around $400k and a typical Australian borrower is likely to change their loan every 3-4 years. Unfortunately, many lenders increase your interest rates the longer you stay with them. i.e. NEW customers are able to take advantage of ‘special’ rates that you can’t access. So let’s look at some examples to see at what point it does become worthwhile changing your existing lender: Repayments on an average $400k loan. Let's look at monthly repayments for a loan with a 3.5% interest rate as a minimum. I would be horrified to think that anyone is paying 5% (unless extenuating circumstances like a low credit score) so let’s use that as a maximum and go from there.   So, if you are still following me, using this second chart, with a $400k loan, covering at least the costs of $600 (but don’t forget there may be an application fee):

If your loan size is $800k, the savings double so you would be in a better position financially in just one year if the new interest rate was 0.11% lower. I think you may be getting the picture. In most cases achieving a 0.22% better rate should be possible but of course it depends on your individual situation and lender preference. There are often ‘specials’ running to encourage you to move lenders and as long as you do your figures (or let me run them for you) you could be better off in a very short period of time. For some of my clients, I have reduced their interest rates by up to 0.8%. With interest rate decreases of that level you could save a whopping $67k on the life of the loan. So in these cases if would be crazy NOT to refinance. But before you jump on the phone and call me to refinance, give your existing lender a call. Tell them that you are looking at moving and ask them if can they do any better than your current rate? If they can – great you just saved money by making one phone call. If they won’t budge at least you know where you stand. Then give me call. I’m a big believer of “if you don’t ask you don’t get”. How complicated is it? Well that depends on many things but very simply if your income, through all sources are more than the loan repayments and expenses combined and you have a good credit record then you should be fine. Before any submission is made to a lender, serviceability is calculated and all evidence is completed reviewed to ensure your loan will be approved before it is submitted to the lender. You don’t want to have any unnecessary credit inquires on your file as every credit inquiry you make impacts your credit score and may not be looked upon favorably by lenders. What do I need to supply to apply to refinance?

You will also need to be ID’ed and provide some information about yourself, your situation and what your aims are now and in the future. I will then complete the applications and any other paperwork required. The whole process takes around 4-6 weeks depending on the lender. Some lenders have a process where the refinance can occur faster through paying out the lender you are leaving first before they transfer the Mortgage as some lenders can stretch this process out causing delays and frustration. So it really isn't as complicated or expensive as you may think. If you have any specific questions don’t hesitate to give me a call. Always happy to have a coffee and a chat and see if I can save you money which is way better in your pocket than the banks! Catherine Thompson is a credit representative 508141 of BLSSA Pty Ltd ACN 117 651 760 (Australian Credit Licence 391237). The information contained in this blog is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice

10 Comments

5/12/2021 04:21:30 pm

It’s cool that you mention that getting a home loan can be good for your credit score when you are purchasing a house. My wife and I want to become homeowners soon, so it would be a good idea for us to get a home loan.

Such a nice and interesting post.

I would definitely recommend this to others.

This is a really wonderful post. I would definitely recommend it to others.

Thank you for sharing this valuable information. I would definitely recommend it to others.

Thank you so much for sharing this valuable information with us.

Thank you so much for sharing this valuable information with us. 9/10/2021 04:47:57 pm

I am so delighted I found your weblog, I really found you by accident,

Excellent post. I LOVE this article! We are a team of expert designers who possess expertise in producing great quality bank statement PDF, bank statements PDF services, paystubs PDF, utility bills PDF and tax returns PDF using your provided documents or creating our own. Because we help our customers to use the bank statements PDF services for educations and entertainment purposes. 10/20/2022 02:29:57 am

Hi there! Excellent post. This topic covered in this is so Amazing & helpful. I LOVE this article! We can help you in getting this work done as we use our own bank statements editing, pay stubs editing, utility bills editing and tax returns editing. And Guys if you want to edit any entries in your Bank or Credit Card Statement? Leave a Reply. |

Message from CAtherineOccasionally I come across an interesting article to do with Home Loans. I thought I'd share some of these with you here. Archives

April 2024

Categories |

RSS Feed

RSS Feed