70% of small businesses number one concern is cash flow. Is cash flow impacting your business in the lead up to the busy Christmas period? Do you need funds to:

And in the meantime, here are some great advice from Business Victoria to address key small business financial concerns. Top tips

1. Cash flow Cash flow is the life blood of business. If your business is suffering from poor cash flow then here are a few things that you could look at:

2. Rising Costs Yes, business costs are rising, but that doesn't mean you can't get a better deal. Try the following:

3. Taxation and business regulation. As taxation and business regulations continue to change it's important to understand how as a business owner you can stay up to date with these changes. A couple of ways to stay up-to-date is:

It's really important to keep your accounting records up-to-date. There is some fantastic cloud based accounting software (such as Xero) which make it so much easier to keep your records up-to-date. Also, talk with your accountant or adviser before you make substantial changes to your business or assets (e.g. buying or selling a property). It's always much easier to plan for change than to try to clean up the mess afterwards. 4. Australian Dollar The rise in the Australian dollar has impacted SMEs across Australia. As movement in the Australian dollar is largely driven by global factors it is difficult to determine how long it will stay at current high levels. If you are an importer, you are no doubt happy with the high dollar, but how will your business perform if the dollar drops? You need to start thinking about this now. If you are an exporter you will no doubt be feeling the pain. Improving the efficiency in your manufacturing or service delivery will help to reduce costs to offset the impact of the dollar. Determining the profit made in each export market will help you to make decisions as to whether you should ride it out or change strategy. If you are going to ride it out, then work closely with your export customers on ways in which you can add value to improve price to offset the impact of the higher dollar. 5. Interest rates The final financial problem SMEs around Australia are concerned about is fluctuations in interest rates and the impact of these movements on their business and lifestyles. While rates are relatively low at present, it might be a good time to think about fixing the interest rate on some of your debt. Fixing the interest rate on your debt generally means that you are not able to pay off the debt faster than the agreed term, so it may be wise to fix the interest rate on a portion of your debt. This will give you some flexibility to pay debt down faster if needed. As a business owner, you should also be aware of how increasing interest rates will impact your business. Including some scenario planning with your budgeting and forecasting is a good idea. This could be a simple as looking at the profit budget and cash flow forecast using a range of different rates. Planning early will mean that you are ready to act quickly should there be a sudden movement in interest rates. If you don't have a cash flow forecast already, read our cash flow forecasting page.

0 Comments

The hidden danger potentially stopping you from owning your own home.

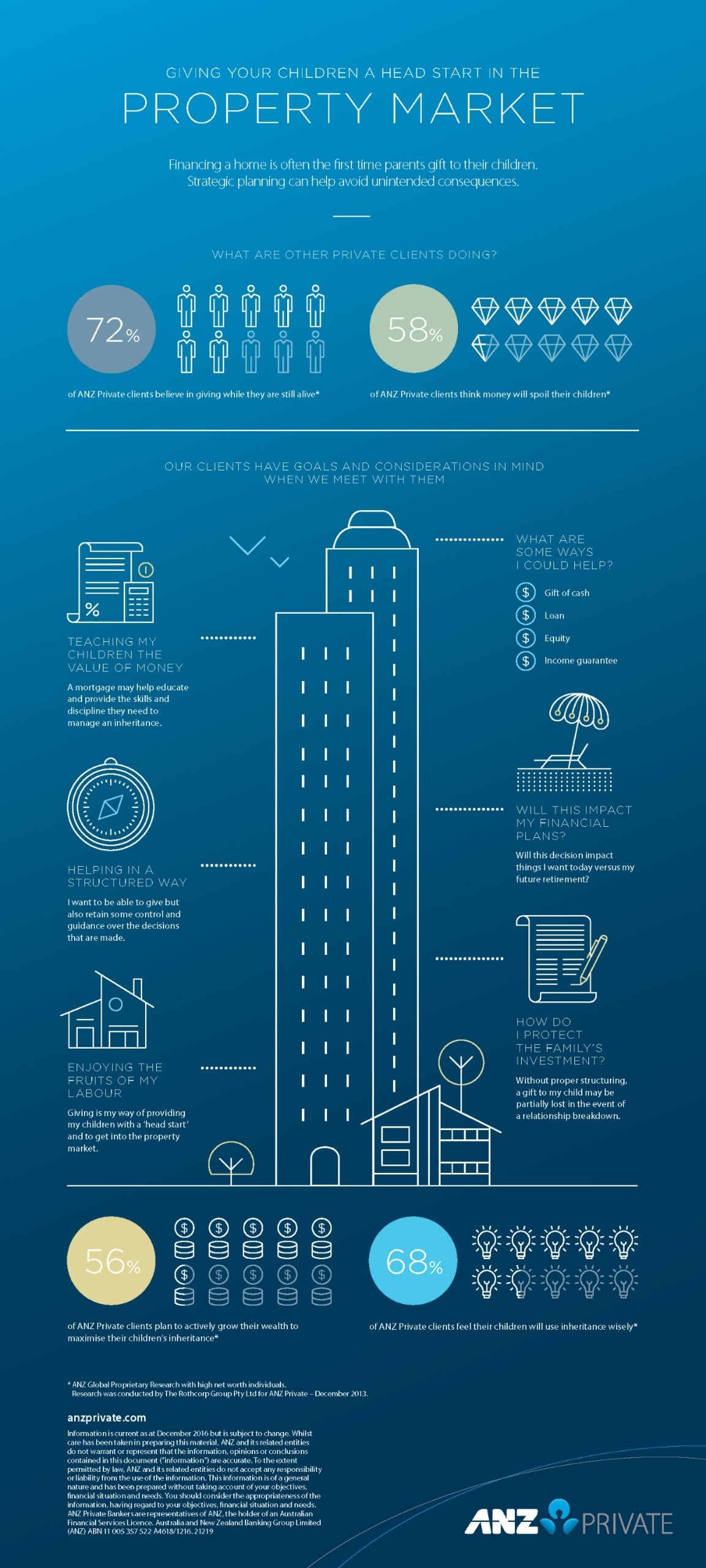

The Buy Now Pay Later sector is winning-over the youth demographic with the promise of instant gratification, but be careful. ‘Buy Now Pay Later’ providers such as AfterPay and Zip Pay have experienced massive growth in popularity, with the number of users jumping from 400,000 to approximately 2 million between 2015 and 2018. Driven by a simple proposition whereby the Buy Now Pay Later provider pays the merchant on behalf of the customer, allowing the customer to obtain the goods or receive a service immediately while subsequently paying off the debt generally through instalments, Buy Now Pay Later presents a tempting offering. But as the sector’s breakneck growth continues, mortgage professionals are warning users, particularly in the younger demographic, to be cautious of overdoing it as this could risk effecting their chances of securing a home loan further down the track. It’s the layby of our day but in reverse. It’s your forward credit for an item, which in theory, can make sense. You get the item or service and pay it off over instalments, so you’re actually putting forward your liability. This might be ok for someone that manages their money well, if they pay off the item on time and use their mortgage offset account correctly. This way they’re delaying expenses and offsetting more of their savings against their home loan. But how many people actually do that? Not many, and the rest are spending beyond their means. As a broker I feel that this method of purchasing may send the wrong message to a bank. If a lender sees a ‘buy now pay later’ provider frequently on a client’s bank statements, that can trigger more questions about their spending behaviours and ultimately may mean they choose to decline the application. Especially if you don't have much savings to support this theory they may have. I would much prefer to see my clients save for the item and demonstrate those good habits. If you are concerned about your level of expenditure or your ability to secure a home loan, come and have a conversation with me at Volare Home Loans and I can set you on the right path. It’s really important to appropriately manage your expenses well in advance of applying for a home loan, that way you can show the bank that you can save and afford to service a mortgage when the time comes.  I often hear parents lamenting about how their children will never be able to afford to buy a house. There are some ways you can help them get a foot on the property ownership ladder. This article goes through the pros and cons of some of these options. The article is courtesy of ANZ (one of the lenders on our extensive panel) and you can read the full article at https://www.anz.com.au/private-bank/insights/planning/helping-your-children-buy-a-home/ “A lot of young professional couples have the repayment capacity but not the saving capacity to buy their first home,” says Queensland University of Technology Professor in property economics Chris Eves. “If parents can help them get the deposit they may be able to move into a purchase decision.” Parents who have the financial means often find satisfaction in transferring wealth to their children during their own lifetime by helping them to buy a home. Those with property experience can play a useful role in guiding their children toward home ownership and helping them determine what is affordable, Eves says. But he advocates leaving the choice of property to the child. “[Generally] the decision has to be the child’s for there to be some level of ownership – parents should realise they’re not living in the property so it should be the child’s taste not theirs,” he says. The level of input parents have into the purchase decision usually depends on how much they contribute financially. Some offer a deposit before stepping back. Others provide significantly more and have a greater say. Many parents helping their children to buy usually favour properties they consider to have the potential for long-term capital gain. Most prefer freestanding houses or townhouses with land, typically within 10 kilometres to 15 kilometres of the city, or located close to family. Before you help even with financial assistance, most young people buying a home need to take out a mortgage. Come and speak to Catherine at Volare Home Loans and she can assess your their borrowing capacity, A good starting point for parents is to see a financial advisor to determine how much to provide. Parents, before helping their children, have achieved their own financial goals such as:

Parents with more than one child may need to consider whether they will be able to provide similar assistance to each of their children. The next step is to decide how to provide the funds. Financial, legal and tax advisors can help determine the best approach, addressing questions such as:

Gift? Often the simplest option is to gift money. Give the child an amount – enough for a deposit or substantially more – where there are no strings attached, There are generally few tax consequences for either parent or child with a gifted sum and there may be no legal structures to establish. (Parents should seek professional advice to confirm the implications of a simple gift.) The biggest drawback is that parents have no right to reclaim the money at a later date. This may lead to regrets if the child’s marriage or relationship breaks down, as the child’s partner may be entitled to half of the assets, including the gifted sum. Similarly, if the child has a business that fails, creditors may be entitled to those funds. Loan? Lending to children can achieve a similar outcome to gifting but with greater protection, says Brennan Solicitors’ Paul Brennan. By structuring financial assistance as a loan – even if the parents do not intend to ask the child to repay the debt – the parents have the option to recall the money. Reclaiming the money would allow the parents to return it to their child later on, after the reason for recalling it has been resolved. A loan can be forgiven on the parents’ death. But establishing a loan is more costly than gifting money. “You generally should have it documented,” says Brennan. “An undocumented loan is a difficult thing because it’s almost impossible to get the money back.” It may also be important to have the loan secured by an asset to help ensure funds can be made available to repay the loan if required, Brennan says. Guarantor? Another way parents can help is to guarantee the child’s mortgage. This allows parents to provide assistance without giving cash up front by using their own income or the equity in their property to secure the child’s loan. A guarantee may allow the child to borrow more than they otherwise could. It may also allow the child to avoid having to pay lenders’ mortgage insurance, which can add tens of thousands of dollars to the purchase cost. If the home rises in value, the child may be able to refinance so the parents are no longer providing security. The risk with this option is that if the child defaults on the loan, due to losing their job, accident or illness for instance, the parents are left having to repay it. Another risk is that if the child buys the property in joint names with their partner and the relationship fails, the child could lose half the house but the parent would remain guarantor for the full value of the loan. Parents should also be aware that acting as guarantor affects the amount they can borrow for other purposes as lenders consider guarantees as borrowings when determining how much to lend. Buy together? Some parents buy in partnership with their child with the intention that the child could buy them out at a later date to take full ownership of the property. The property may be owned directly or through a trust. This may suit some families but is generally not popular. If you do this, the child won’t be able to get any first-home-owner grants. Also, if it’s going to be the child’s own residence, they don’t have to pay any capital gains tax but the parents will have to. If the parents are buying in partnership with their child, they should consider buying in joint names or through a family trust so the property would transfer seamlessly to the child on the parents’ death. Refer to the infographic from ANZ Private Bank below to consider ways you can assist your children in buying their first home. If you have any questions or would like to discuss this any further please call Catherine on 0411 849 804.  Our friends at financewomen have pulled together some simple but effective ideas for the new financial year:

2. Get a better deal

A small change to some of your bigger expenses can make a huge difference to your cash flow. By checking out better deals on your mortgage (let me do this for you) you might be able to save even a quarter of a percent. On a $400,000 mortgage that saves you $1,000 a year. By knowing what other lenders will offer you can even approach your existing bank and ask them to give you a discount to stop you moving, might save you both money and hassle. Choice’s new research has estimated that switching your shopping from Woolworths and Coles to Aldi can save you 50% off your grocery bill. A typical family can easily save $100 a week on the grocery bill, a whopping $5,000 a year. As a fairly passionate Aldi shopper for the past couple of years I have been really impressed by quality of the meat and veges, not just the packaged goods. It takes a while to get used to their range and for particular specialty or branded items you might need to duck into a rival to complete the list every now and then, but the range at Aldi is getting better and better and I’m finding much less reason to shop at the big two these days. For me it’s time to revisit my electricity deals. Since I last did this the Victorian State Government has introduced a couple of really nifty measures. I plan on claiming my $50 bonus when I use the independent comparison tool to find out the best deal for me. Furthermore I’m fairly impressed at their new Default Offering which is mandating a fairer price for those consumers who have been a bit disengaged and may not be getting a good deal on their electricity prices. If you live in Victoria you might like to check out the Victorian State Government’s programs including the $50 rebate and comparison tool. 3. Making the most of your tax refund If you are lucky enough to get a tax return this year, what are you going to do with it? If you’re like most of us it either goes on a bit of a splurge or disappears into the vacuum of your bank account never to be seen again. How about using it a little more constructively this year? You don’t need to be a complete miser though. How about agreeing now that half is you to enjoy now and half later. When you’ve worked out how much it’s going to be, be disciplined about both the spending and the saving. Make sure you enjoy your ‘now half’ whether it’s the size of a dinner or a new handbag or only stretches to that book you’ve been promising yourself or a ticket to the movies. Then make sure that you deliver on your commitment to enjoying the ‘later half’. You can make an extra contribution to your super or into the part of your mortgage you can’t easily get your hands on. While your doing you your tax return this year keep one eye on what you could do better for the next year. Is it keeping receipts when you donate money? Or keeping a log bog for your car mileage? What can you do now to make next year’s tax time easier and more rewarding? So you’ll have more money for now and later next year!

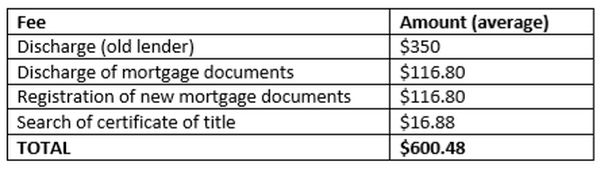

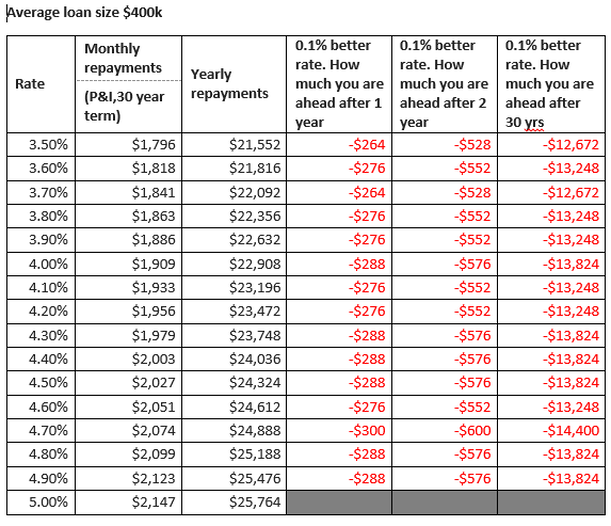

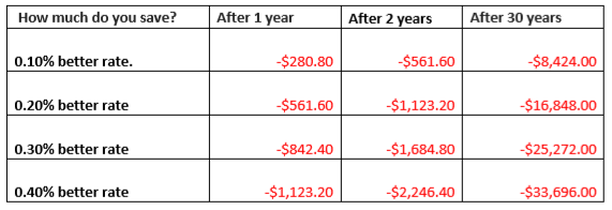

by Catherine Thompson - Principal of Volare Home Loans  Many people I talk to aren’t really sure what’s involved in refinancing a home loan. Does it cost a lot? Is it complicated? Is it worth it? Does it really save me money? If you'd like to know more, keep reading. If you don’t like reading, give me a call and I'll talk you through what's involved! Let’s start with the costs involved While the costs aren’t significant, they do exist. Most lenders will have a Discharge fee which is typically around $300-$350. Then there are Government fees of around $250. But that’s not all. There could be application fees (but not always) for the new lender and these generally range from $0-$600. Application fees often cover the valuation, legal fees and settlement fees. So, in total you need to be better off by at least $600 plus any new application fee amount to make a change worthwhile.  Now for a few more stats, according to the ABS, the average Victorian home loan is around $400k and a typical Australian borrower is likely to change their loan every 3-4 years. Unfortunately, many lenders increase your interest rates the longer you stay with them. i.e. NEW customers are able to take advantage of ‘special’ rates that you can’t access. So let’s look at some examples to see at what point it does become worthwhile changing your existing lender: Repayments on an average $400k loan. Let's look at monthly repayments for a loan with a 3.5% interest rate as a minimum. I would be horrified to think that anyone is paying 5% (unless extenuating circumstances like a low credit score) so let’s use that as a maximum and go from there.   So, if you are still following me, using this second chart, with a $400k loan, covering at least the costs of $600 (but don’t forget there may be an application fee):

If your loan size is $800k, the savings double so you would be in a better position financially in just one year if the new interest rate was 0.11% lower. I think you may be getting the picture. In most cases achieving a 0.22% better rate should be possible but of course it depends on your individual situation and lender preference. There are often ‘specials’ running to encourage you to move lenders and as long as you do your figures (or let me run them for you) you could be better off in a very short period of time. For some of my clients, I have reduced their interest rates by up to 0.8%. With interest rate decreases of that level you could save a whopping $67k on the life of the loan. So in these cases if would be crazy NOT to refinance. But before you jump on the phone and call me to refinance, give your existing lender a call. Tell them that you are looking at moving and ask them if can they do any better than your current rate? If they can – great you just saved money by making one phone call. If they won’t budge at least you know where you stand. Then give me call. I’m a big believer of “if you don’t ask you don’t get”. How complicated is it? Well that depends on many things but very simply if your income, through all sources are more than the loan repayments and expenses combined and you have a good credit record then you should be fine. Before any submission is made to a lender, serviceability is calculated and all evidence is completed reviewed to ensure your loan will be approved before it is submitted to the lender. You don’t want to have any unnecessary credit inquires on your file as every credit inquiry you make impacts your credit score and may not be looked upon favorably by lenders. What do I need to supply to apply to refinance?

You will also need to be ID’ed and provide some information about yourself, your situation and what your aims are now and in the future. I will then complete the applications and any other paperwork required. The whole process takes around 4-6 weeks depending on the lender. Some lenders have a process where the refinance can occur faster through paying out the lender you are leaving first before they transfer the Mortgage as some lenders can stretch this process out causing delays and frustration. So it really isn't as complicated or expensive as you may think. If you have any specific questions don’t hesitate to give me a call. Always happy to have a coffee and a chat and see if I can save you money which is way better in your pocket than the banks! Catherine Thompson is a credit representative 508141 of BLSSA Pty Ltd ACN 117 651 760 (Australian Credit Licence 391237). The information contained in this blog is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice

The goal is to be rich not look rich. This has come to be one of my favourite sayings. The number one reason why wealthy people are wealthy is because they watch what they spend their money on. Here are some ideas:

1. Live below your means (NOT just within your means) Just because your friend Jo eats at expensive restaurants every day, buys the lastest iPhone or new car just after it's released, doesn’t mean you have to. The best way to ensure you are wealthy later on in life is to live below your means now. Be aware of what it costs you to live and stay within those limits. And definitely do not using credit cards or loans to maintain a lifestyle to compete with others. 2. Eliminate unnecessary expenses Do you buy lunch everyday? get UberEats all the time? catch an Uber instead of public transport or walking? These are all unnecessary expenses that simply require a little planning to not utilise. Your health and wallet will thank you. 3. Do It Yourself (DIY) Do you really need to get someone to do your gardening, wash your clothes, clean your house, wash your car, wash your pets, deliver your food? The money you spend paying for these services could redirected to saving or investing. 4. Sell the stuff you no longer use How many things do you have lying around that you could list on eBay, Gumtree or FB Marketplace. Thanks to all these platforms and more, you can sell these items and not only clear out your house, you may be surprised at how much you can make. 5. Find a side gig With platforms such as AirTasker, Uber and fiveer, consider a part time second job or side hustle for some extra money. Or create your own website/Instagram page and sell your services/products for some extra cash. It is important to remember that becoming rich is a slow process that requires you to be disciplined, focused and patient. It will be worth it in the end.  Since 2004, Heartland has assisted over 17,000 Australians aged 60 and over release equity from their home, helping them to live a more comfortable retirement, with independence and dignity. However, some misconceptions regarding what a reverse mortgage is, and how they work, persist. Watch the video below to debunk three common reverse mortgage myths: Did you know that reverse mortgages are one of the most heavily regulated consumer finance products in Australia? The Heartland Reverse Mortgage has a number of protections to provide you with maximum peace of mind. These include:

As you can see, our reverse mortgage has been developed with customer protection at its heart. Read more about these protections on our Borrower Protection page. Alternatively, if you'd like to talk to a Accredited Authorised Broker contact me on 0411 849 804. I'd be only too happy to discuss any questions you may have.

Don't pay more than you have to

Make small changes in your home

Autumn is the time to prepare your home so it can keep you warm throughout winter without the bills that come with it.

Just like getting a job in your 50's, getting a home loan can require some planning. Come and have a chat with me and we can put some plans in place so you will be approved at your first choice of lender. I hope you pick up some useful tips from this article. Catherine BY ANNE MOLLEGEN SMITH Becoming someone who’s readily employable in your 50's (and beyond) calls on a skill set you can and should start working on as early as your first few jobs – even when you’re just in your teens or 20's. You can also pick up and start polishing these strengths, even if you’re in your 60's or 70's when you want to find work. Today people can expect to have as many as 11 jobs over a career lifetime. With a tip of the hat to the late Stephen Covey, you might think of the following as the “Seven Habits of Highly Employable People.” None of the skills we’re recommending should be cultivated in place of competence in your work or loyalty to your tasks; rather, these are the extra things that will make you more hirable on top of your other abilities. Each general point is paired with age-specific recommendations for when you’re in your 50's, plus some key moves to immediately make if your job search is in high gear or you’re suddenly out of work. 1. Cultivate Friendships, Not Just “Networks” LIFELONG HABIT: Forget self-conscious networking. Instead, concentrate on making friends and on being a friend. Take an interest in other people, remember their stories, stay in touch, send thank-you notes and celebrate people’s successes. Be the friend you’d like to have – loyal, generous and trustworthy. Take small social risks: Invite people to join you in something, offer a ride home, learn to accept help and be generous with your time. In your 50's: Include younger people among your friendships as well as the older and more powerful people who can help you now. Like networking, “mentoring” has become a cynical cliché, but inside the phony stuff is something valuable. Make a point of spending some time with younger colleagues and people in your area, but be careful that you listen to their concerns more than you preach to them. As your friends’ children come of age, take an interest in them, too. Searching in high gear: If you’re still employed but actively looking, now’s the time to contact recruiters and mark what you send to HR departments as confidential. Be sure your resume is up-to-date, not just in terms of your work history and career objective, but also in its format: Is it scannable in an Applicant Tracking System (ATS)? Have you embedded the current buzzwords for the jobs you’d like to get? Shorten the older items on your resume and delete any job duties that will make you seem too old-school. If nobody uses whizamajigs anymore, then don’t list that you’re good at them. (See 7 Ways Your Resume Dates You for more.) Consider having a personal web page and develop your capsule self-description. Urgent: Work on a simple explanation of why you’re out of work that is basically true and doesn’t reflect too badly on you, on your ex-boss or on the company. Refine and rehearse it until you can say it without getting upset. This is not the time to have axes to grind. You may want to vent to close family and a few patient and loyal friends. Until you can get your emotions under some control, though, stay off the phone and watch what you put in the e-mail and what you say in public. When you go out socially, be careful that having a drink or two doesn’t loosen your tongue, release your anger or bring out self-pity. Be ready with small-talk topics so that you can deflect the conversation away from yourself. You can now send out another round of resumes to say you’re available immediately or a month or two in the future. Update your LinkedIn profile. (See How To Use LinkedIn To Get A Job.) 2. Keep Up Your Looks, Your Spirit And Your Energy' LIFELONG HABIT: Stay fit – exercise enough to sleep well, have plenty of energy and stay healthy. Control your weight. If stress is a problem in your life or work, make changes. Don’t hover between a rock and a hard place; figure out a better spot and move toward it — even if it’s a lateral move. Avoid unnecessary financial stress, which usually boils down to: Live enough below your means to prevent financial problems, build up an emergency fund and set aside regular savings for future goals and needs. In your 50s: Periodically evaluate your wardrobe and your overall style. Get rid of clothes that look dated no matter how much you liked them when they were new. Is your hair thinning, graying or receding so that it’s time to change the way it’s cut or styled? Be wary of coloring your hair very dark even if that’s your original color; all-one-tone dark hair can look fake and harsh on older faces. Instead, consider using a shade or two lighter to tone down gray without looking like you applied shoe polish to your head. Searching in high gear: You may already be a member of a trade association or civic organization; this is the time to seek a leadership role in it – head an important committee, chair an event or take on a challenge that will give you visibility and favorable word of mouth. Urgent: See if you can negotiate an exit package that not only provides some health coverage, severance and so on but some outplacement perks as well, such as a health or golf club membership, for instance. (See The Layoff Payoff: The Severance Package.) In your professional organization, join an existing committee – any committee – and work your tail off. It’s a good way to boost your reputation as a doer and keep up your self-respect. 3. Have Two Irons in the Fire LIFELONG HABIT: Unless you are the owner of a new business, do not let one job take all your time and energy: You can have a major career and a minor career. At some point, they may flip. Or you may have a two-tier career: Break jobs into tasks – and turn tasks into secondary careers, possibly very part-time. For example: An interior designer with corporate clients also has a local custom-upholstery business with several part-time employees. Your two career lines may be related or completely independent. Today’s trend is toward “slasher” occupations, often in surprising juxtapositions: accountant/garden designer. Jazz drummer/journalism professor/craft beer brew consultant. Church organist/web designer/computer programmer. In big or little ways, what you observe and learn in one job may help you in the other. In your 50s: In most families, this time of peak earnings is also a time of high expenditure for children’s college or even secondary school costs, home renovations, parental caretaking and medical expenses. Can you wrest more income from your sideline so that you can keep up your regular retirement savings and keep down overall debt? Whatever your interests and skills are, consider whether you can share or teach them to others as a paying sideline. The church organist may be able to add more weddings to his schedule and teach a few private pupils as well. The local history expert starts giving walking tours and entertaining illustrated lectures for a fee. Searching in high gear: As realistically as you can, size up your prospects. Do you need to relocate? Research areas that might have better opportunities for you. (Some of these Top 10 Cities For Grads To Get Jobs may be good for you, too.) Do you need to take classes toward certification in a specialty? Start now. Do you need to switch to a different career? Get serious. Figure out how you can best use the lead time to lay the groundwork for a career transition. Urgent: Maybe you can rustle up some short-term projects while you finish a degree or hit the ground jogging in the new location by doing some temp work. But don’t be afraid to think long term. The rate of increase in labor force participation by people 65 to 69 continues to grow every year and is expected to reach as much as 36.6 percent by 2026. 4. Make Yourself a Pleasure to Be Around LIFELONG HABIT: Be gracious, grateful and generous. If you have problems with depression, anger or anxiety, deal with them. Get help, including short-term therapy and/or taking necessary prescribed medication when your demons get the upper hand. Learn to shed your grudges. Remember, chronic anger and anxiety will show in your face as you age, making you easier to read and harder to like. Learn to ask people easy social questions rather than talking about yourself too much, and try to show a sense of humor about yourself. Share news but not unkind gossip. Even if no one’s looking, don’t kick the neighbor’s cat. In your 50s: You may be facing up to the limitations of your body for the first time, but do not make it a mainstay of your conversation. No need to joke about “senior moments” when you can attribute memory lapses to “multitasking overload.” If you face a health problem, focus on recovery or management of it. In short, don’t get hung up on aging as a problem. Searching in high gear: Convey open-minded, positive expectations of the next phase along with a readiness to move into it. Show that you’ve enjoyed your work in the past, not just the paychecks. Don’t try to hide or lie about your age – that is, don’t treat it like a dirty secret, just redefine it as if to say, “My age 55 is as full of energy and optimism as age 40, but look how much smarter and wiser I am now.” Urgent: If you’re getting the interviews but never the job, and if you think your age is holding you back from work you are qualified for, go to a career coach for help in discarding behaviors you may not be aware of that are weighing you down. But face the fact: Prejudice and age-stereotyping exist in the world, and you cannot control everything from your side of the desk when you’re the one sitting in the guest chair. (Read 5 Reasons You Didn’t Get The Job.) 5. Know Your Business Universe LIFELONG HABIT: Keep up with not only the state of your company but of the industry as a whole. Read the business and trade press; follow the important blogs. Join industry forums and groups online. In your 50s: Make note of which companies would be the best to work for, who the leaders are, and also who is likely to be one of tomorrow’s stars. Keep bookmarks or a clip file. Go out of your way to get casually acquainted with influential people in your field that you don’t already know. Searching in high gear: Turn that casual knowledge into an action list. Contact people, suggest having lunch or coffee and out of the corner of your eye, start paying attention to what’s happening in other fields you might transition to if things come up dry in what you’ve been doing. Urgent: Has someone relevant to your search recently appeared in the trade press? If it’s favorable, you can mention it in a cover note or in person. 6. Keep Learning LIFELONG HABIT: Read books, go places you’ve never been, expose yourself to different ideas and cultivate additional skills. Be curious and at least a little adventurous about what’s new. In your 50s: Sign up for a massive open online course (MOOC), take online tutorials, add some digital skills and make use of various life hacks. Listen to TED talks, take voice or yoga classes. Get out of your comfort zone sometimes. Do things you enjoy and challenge yourself with new stuff. Mix socially with people of all ages, but especially arrange to have contact with people 5 to 10 years younger than you or more. Committee work or nonprofit volunteering is one good way. Among other things, this will update your conversation with current references and catchphrases. Searching in high gear: Embrace the 21st century – use all the digital support you can get. Visit online job-search sites: Check out Indeed.com, Career Builder, ZipRecruiter.com, Glassdoor.com and Freelancer.com. Look at Idealist.org for nonprofits. Which sites fit your needs? Ask other people in your field for suggestions – especially those who’ve recently changed jobs. Urgent: Sign up to teach a course or just a single class that will give you a good reason to visit people who might be in a position to hire you in the near future. Ask them what your students need to know. Position yourself as someone comfortable in a leadership role whether in a classroom or the workplace. Besides, who isn’t flattered by being interviewed as an industry leader or knowledgeable person? Now that it’s no secret you’re looking, update your LinkedIn profile with whatever you’re teaching or lecturing about; pull out a couple of points to highlight. Add other recent accomplishments and adjust the setting so your update goes out to your full list of contacts – but don’t do this trick too often or you’ll become a bore. 7. Accept Feedback Without Getting Defensive LIFELONG HABIT: If this is hard for you, get some practice by taking a few courses outside of work. Or take up a new sport; getting coaching will help you if you need to learn how to learn. In your 50s: Abandon false pride: If you get passed over for a promotion or a job you thought you were qualified for, try to find out why so you can fix the problem. Be careful not to appear as though you have a chip on your shoulder. As long as you can keep learning and changing, you’ll never be a has-been. Throughout the job search: Think of this period like staying in training for a sports competition or having your home on the market so you can’t permit personal “stuff” like laundry (or self-pity) to pile up or leave dirty dishes (or disgruntled attitudes) out on display. The Bottom Line - There are reasons some people seem to float easily from job to job as though jobs come looking for them rather than the other way around. Develop and practice these “Seven Habits of Highly Employable People,” and you'll improve your chances of becoming one of them. Today, being in your 50s is certainly not too late to put new habits into practice because you may have another 10, 15 or 20 years to go in your career – and they may as well be good ones. |

Message from CAtherineOccasionally I come across an interesting article to do with Home Loans. I thought I'd share some of these with you here. Archives

April 2024

Categories |

RSS Feed

RSS Feed